June 2021 economic review

Economy partly on right track, but lockdown level 4 back

At the beginning of June, US employment data was released showing that this economic giant’s unemployment rate fell to 5.8%, slightly better than expected and below April’s 6.1%. The US hospitality sector again led job creation, with 292 000 new positions.

A stream of good news in June

Locally, economic output as measured by GDP grew by 1% (an annualised 4.6%) in the three months through March from the previous quarter. However, year-on-year GDP contracted 3.2%, which means output is still down from a year ago. In a surprise move that bodes well for future long-term GDP and the burden on tax payers, the government announced that it will increase the generation threshold for companies to produce their own electricity without a licence to 100MW. This announcement came in the same week as the sale of 51% of South African Airways (SAA) to a private flight operator.

According to the BER Bureau for Economic Research, retailer confidence leapt to a six-year high of 54 points in the second quarter. That’s up from 37 points in the first quarter. Consumer inflation accelerated to 5.2% in May from 4.4% in April, The biggest driver of the increase in CPI is the price of fuel, which is 37% more expensive than it was a year ago. Also during June, Naspers’ annual results showed that company revenue grew by 32% to $29.6 billion and trading profit increased 45% to $5.6 billion.

High SA joblessness exacerbated by level 4 lockdown

Clouding the stream of good news in June was South Africa’s employment data release. Unemployment has risen to a new record high of 32.6% in the first quarter of 2021. Most of the job losses were in construction. And towards the end of the month came the president’s announcement that SA is about to re-enter lockdown level 4 with amended restrictions, effectively closing down alcohol-related industries, hospitality and tourism.

Global equity not losing any steam in June

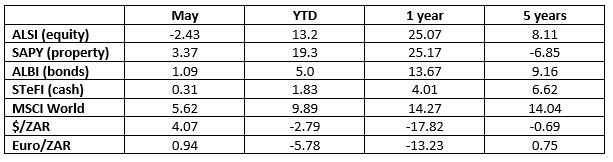

The MSCI World index (developed market global equity) returned 5.62% in rand terms for the month of June. The rand weakened 4.07% against the US dollar and 0.94% against the euro. SA equities as measured by the FTSE/JSE All Share Index (ALSI) lost 2.43% in total returns for the month. The local listed property sector (SAPY) had a positive return of 3.37%. SA bonds (ALBI) gained 1.09% during the month and cash (STeFI) once again returned 0.31%.

One-year returns are off a low base

Since last year’s market lows, most indices have recovered well. The ALSI returned 25.07% for the year to end June. Listed property gained 25.17% for the past year. The ALBI returned 13.67% for the year, and cash gave 4.01%. The rand strengthened 17.82% against the US dollar and 13.23% against the euro over the 12 months to end June. The MSCI World Index gave South African investors 14.27% in rand terms.

Over five and ten years, global equity is still ahead

Over the past five years to June 2021, the ALSI returned 8.11% per year (but over the past 10 years this figure stands at a more acceptable 10.92%). As the worst performer over the most recent five-year period, listed property (the SAPY) returned -6.85% annualised (4.2% over 10 years). Bonds, at 9.16% returned more than local listed equities over the past five years, but lags equity at 8.53% over 10 years. Cash gave 6.62% p.a. on average over the past five years and 6.26% p.a. over 10 years. The MSCI World Index (developed market equities) gave a 14.04% p.a. total return in rand terms over the past five years and 19.2% p.a. over 10 years, comfortably beating all major SA asset classes.

Table 1: Total returns to 30 June 2021

Source: Morningstar | Total returns annualised to 30 June 2021

Share On:

Comments are closed.